Exploring the Carrier Underwriter Mindset: Why They Ask The Things They Do

Simply put, insurance is the business of assessing risk. As regards lawyers professional liability coverage, insurance carrier underwriters explore the risk profile of a particular law firm through a multitude of variables. Each carrier looks at these variables with a nuanced eye as well as a set of underwriting guidelines that are specific to that carrier. This uniqueness is predicated on their own loss history and experience. Nonetheless, there remains a commonality of broad based criteria that each carrier addresses as to a law firm. This article will seek to explore this process through the mind’s eye of a carrier underwriter who has just received a submission for coverage.

The Application

The application for coverage provides information to the underwriter to assist them in determining whether the insurance company wants to take the risk and provide coverage for the firm. The reliance of the underwriter on the information contained in the application and supplements is so important that both become part of the policy and “insurance contract”. The firm should absolutely view the whole process as a necessity which forces you to take the time to review all aspects of the firm’s practice. So while it is a time consuming task, the execution of the application is an important step which allows the firm to advocate for itself while seeking the most comprehensive coverage at the most competitive premium.

Name of the Lawyers

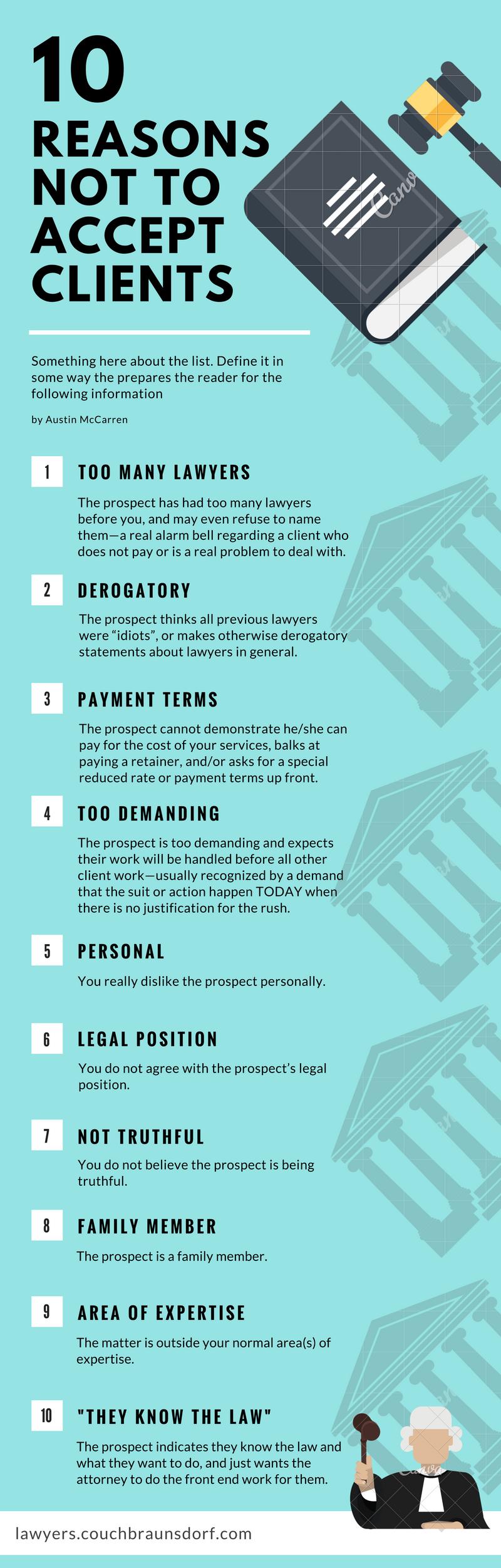

The company is watching for names which may include other businesses that the attorneys own or operate in addition to the practice of law. These entities may need to be excluded. The underwriter will look for potential prior submissions from a firm to assess whether it was approved or declined in the past and if so for what reason. Any exposures reported on the previous application and now shown again will be investigated if pertinent. The address will also be examined for out of state locations. If out of state, which state’s policy form and rates will apply? Are there additional offices not shown on the application? The underwriter will inquire as to interoffice time/docket controls, staffing and management, derivation of receivables, etc.

The Years of Practice per Lawyer

A comparison will be made between the date of admission to practice and the date of affiliation with the firm. The underwriter will also check to be sure that information is supplied for all attorneys listed on the letterhead. This is where questions about “of counsel” attorneys often come up. Do you want to cover this of counsel attorney or is the position largely ceremonial? If you desire to cover this attorney then what are his her or her hours per week on behalf of the firm? This may result in a reduced pro rata premium for that particular attorney. The names of the firm attorneys may also trigger a comparison to a declination list maintained by the carrier. Does the firm seek prior acts coverage for all attorneys or is coverage desired as of a particular lawyer’s date of hire. From a risk management perspective, this may allow the firm to control its exposure from a lateral hire’s prior firm. Its risk profile may be viewed more positively and its self retention (deductible) exposure protected if an attorney is covered as of their particular date of hire.

Support Staff Utilized

Most policies are designed to cover all employees normal to a law firm for their duties on behalf of the firm. No premium is charged for this exposure. Underwriters will look closely at a sole practitioner to determine whether there is a secondary person responsible for maintaining the firm’s time/docket control system to ensure that proper attention is paid to statutory filing and discovery compliance. The more the firm can elaborate as to its secondary systems or one that may have been recently implemented, i.e. PC LAW, NEEDLES, the greater the potential for further premium credits. Underwriters will also look at whether the number of firm employees is excessive and disproportionate when compared to the number of actual attorneys at the firm. This may indicate whether too much legal work is being delegated to non-attorneys without adequate supervision. Law firms engaging in collections practice are particularly scrutinized as to this staff to attorney ratio as underwriters are sensitive as whether it is law firm engaged in the practice of collections law or whether it is a collection agency.

Areas of Practice

Underwriters consider certain areas of practice high risk and may require special underwriting considerations such as a reduction of limits, higher deductible, reduced credits, restrictions in coverage, etc. Certain practice areas require more stringent time/docket control systems or trigger a supplemental application. These are designed to drill down further in exploring those areas of concern to the underwriter. Plaintiff’s personal injury, real estate, banking & financial institutional work, intellectual property for example will require greater underwriter scrutiny which in turn impacts availability of coverage and/or pricing. Other practice areas such as criminal defense, insurance defense or immigration work are considered low exposure which in turn triggers premium credits. Use this as an opportunity to educate the underwriter on how well your firm manages its practice. Descriptions of safeguards or loss control measures show the underwriter that your firm is aware of the risks and has planned for particular contingencies. Of particular importance regarding firm practice areas is the firm website. While ostensibly a marketing tool, it is incumbent upon the firm that it not puff its areas of practice capabilities. If you are a personal injury practitioner engaged largely in auto or premises liability cases, avoid presenting yourself on your website as a medical malpractice or wrongful death practitioner so that underwriters view you as a more favorable risk.

Description of Docket Control and Conflict Avoidance Systems

Underwriters want to know how a firm manages the South Carolina business insurance. The internal procedures are just as important to the issue of insurability as the firm’s substantive expertise and proficiency in the various areas of practice. Premium credits or debits may be applied based on whether the firm has adequate docket control and conflict check systems. A firm should use this opportunity to further elaborate and describe its respective system, i.e. the aforementioned PC LAW, NEEDLES or perhaps an ABA approved or sponsored program. Such attention to detail may result in further premium credits.

Claims History

The carrier underwriter is doing two things when reviewing claims history. First, they want to make sure that all suits and potential claims have been reported to the applicant’s current carrier, if applicable. No carrier wants to provide coverage for claims or potential claims which the applicant is aware of prior to becoming an insured. They will not inherit a lawsuit. Also, the carrier wants to review the claims history to determine whether this been a profitable account in the past. This is the firm’s opportunity to “elaborate & advocate” for itself. A thorough explanation of frivolous claims is really helpful as it gives the underwriter a reason to not decline the account or alternatively debit the premium. If there are substantive claims, it is incumbent that the firm thoroughly describes subsequent remedial measures implemented to avoid repeat claims. Again, carriers are in the business of assessing risk and as such the firm should use this opportunity to advocate for itself.

Conclusion

Securing the most comprehensive professional liability coverage at the most competitive premium should be a critical component of every law firm’s internal risk management process. From the perspective of the carrier underwriter, albeit a person with very little if any exposure to the applicant firm, the application itself for professional liability insurance coverage becomes a snapshot into the law firm’s soul. The firm in turn must treat the application process with respect, thoroughness, honesty and proper importance. Coverage viability and firm economics will depend on that vigilance!

Read More.

We are always here to help you.

-

Visit Us

701 Martinsville Rd. PO Box 888

Liberty Corner, NJ 07938 - Email address gpinckney@couchbraunsdorf.com

- Call now 908 660 0225